The Wednesday Weekly

Financial Market Insight February 18th, 2026

Weekly Market Insight

Welcome to our weekly market update. This newsletter is designed to provide you with current market data, investment insights, and educational information about market trends and strategies. The content herein represents our observations and analysis of market conditions and is intended for informational and educational purposes only. It does not constitute personalized investment advice or a recommendation for any specific security or strategy.

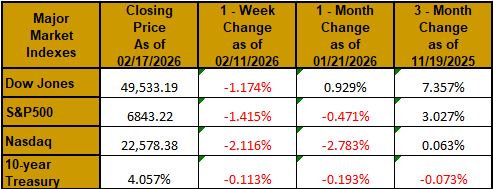

Major Market Indexes

Closing Price as of 02/17/2026

The Strong Tower Difference

Ask Yourself…

What do you own?

Why do you own what you own?

Do you know what you’re truly paying for your investment management and advice?

If you can’t answer these three questions, watch this video.

Current Items of Interest

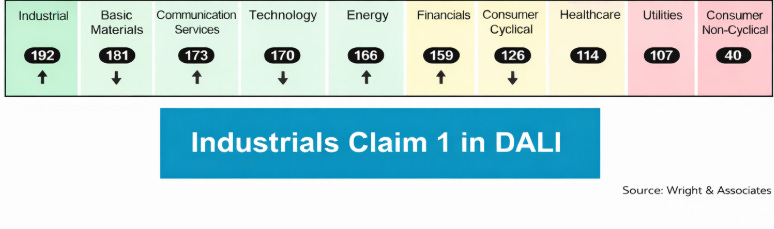

Sector Rotation Update

Major tech firms, including Microsoft, Alphabet, Amazon, and Meta, are expected to spend over $600 billion on AI in 2026, requiring heavy investment in data centers, semiconductors, and energy systems. While this spending supports long-term AI growth, it reduces near-term financial flexibility, potentially limiting buybacks and increasing debt. As a result, capital has flowed toward infrastructure-linked sectors such as energy, industrials, and materials, which have led market performance year-to-date, while technology and related growth sectors have lagged. Overall, AI’s expansion still relies heavily on traditional industries, creating a meaningful rotation in sector leadership.

AI Infrastructure Beneficiaries by Sector:

Energy & Power Generation

Industrials & Electrical Infrastructure

Materials & Critical Inputs

Data Center Real Estate

The Case for Cutting Rates

Cooling inflation is strengthening the case for potential rate cuts. The latest Consumer Price Index (CPI) from the Bureau of Labor Statistics came in slightly below expectations at 2.4% year over year, helping lift market expectations for easing at the June 17 FOMC meeting. As prior tariff-related price pressures roll out of the 12-month calculation window, inflation readings may continue to moderate, further supporting the possibility of lower policy rates. Following the CPI release, rate-cut probabilities rose modestly, and fixed income markets responded positively. The Federal Reserve rate outlook has improved the backdrop for bonds, including the iShares US Core Bond ETF (AGG), which saw renewed demand for buying. While fixed income currently ranks weaker compared to equities on a relative strength basis, a more constructive rate environment could support performance, particularly in longer-duration bonds. Convertible bonds and long-duration global income strategies may be well positioned, as they could benefit from both falling yields and improving equity trends. Overall, moderating inflation and rising rate-cut expectations are creating a more favorable environment for selective opportunities within fixed income as 2026 progresses.

Volatility Clusters

Volatility clustering is a well-documented observation in financial markets where periods of high volatility tend to be followed by more high volatility, and periods of low volatility tend to be followed by continued calm markets. In other words, market volatility is not random through time, it tends to occur in clusters.

What volatility clustering looks like:

Quiet market environments often persist for months with relatively small daily price changes.

After a spike in volatility (economic crisis, policy surprise, geopolitical event), markets may experience extended stretches of large daily moves rather than a single volatile day.

These episodes can last weeks or even months before volatility gradually declines again.

Why volatility clusters occur:

Several behavioral and structural factors contribute:

Information flow: Major macro or policy uncertainty leads to repeated reviews of investment holdings by investors.

Leverage and risk management: Margin calls, deleveraging, and systematic risk controls can amplify sustained volatility.

Investor psychology: Fear and uncertainty cause “herding” behavior, increasing short-term price swings.

Liquidity conditions: During stress, reduced liquidity makes prices move more sharply, sustaining volatility.

Bottom Line:

Volatility tends to rise and remain elevated during market stress, so risk can remain higher than expected even after the initial decline. Risk-management approaches that adjust exposure during prolonged high-volatility periods may help moderate drawdowns, although they cannot eliminate risk. (Relative Strength combined with an executed Exit Strategy, can be of assistance here.) Periods of unusually low volatility may precede sudden market shifts, reinforcing the importance of diversification and disciplined allocation.

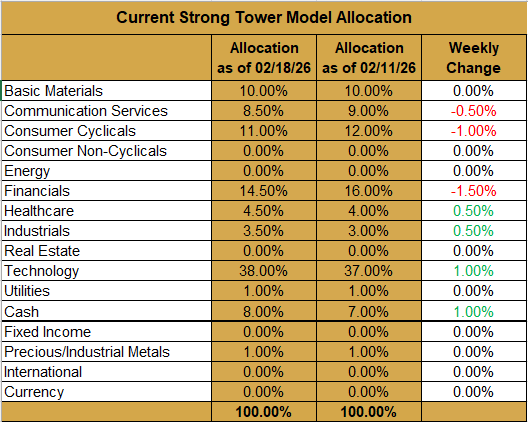

Current Strong Tower Model Allocation

Clients Only — Allocation as of 02/17/2026

Bottom Line:

52.00% of our model is currently in the top 4 Industry Groups.

92.00% of our model is currently in the top 8 Industry Groups.

About Us

At Strong Tower Wealth Management, we offer comprehensive wealth management services using a goal-focused and holistic approach that considers each client’s overall financial situation, including their family, circumstances, and objectives. Our services include investment management, insurance planning, and estate planning coordination, provided with an emphasis on clarity and transparency.

Not a client yet? We invite you to schedule an introductory assessment with Brett to discuss your financial goals and learn more about how we can support you.

Brett Lewis

Founder / Managing Director

Strong Tower Wealth Management

www.strongtowerwealthmanagement.com